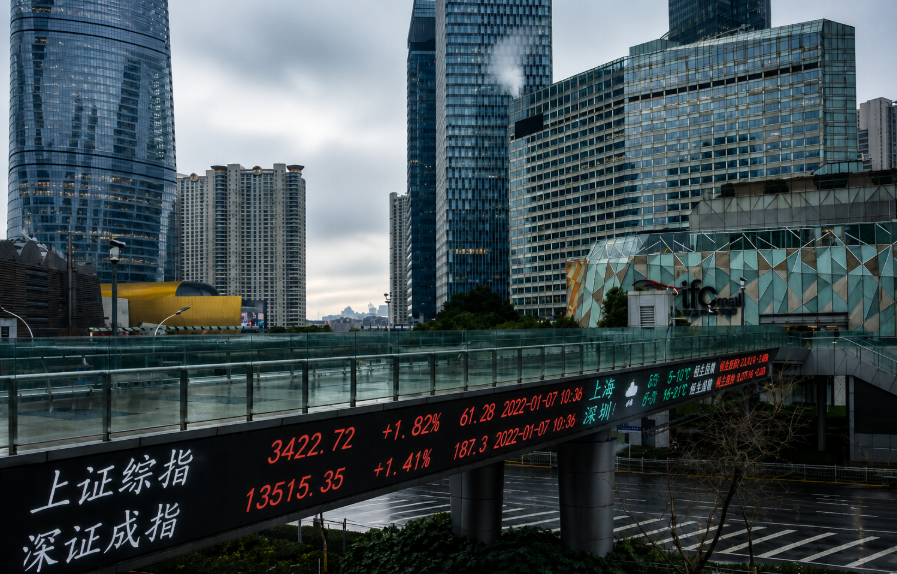

Wednesday, July 1 gave Chinese equity markets a clear reason to move. China stocks rise on robust factory activity data showing seven consecutive months of manufacturing expansion, combined with President Xi Jinping reiterating Beijing's pledge of "high-quality development." The CSI300 large-cap index gained 0.4 percent by the lunch break. The Shanghai Composite Index rose 1.1 percent.

Those numbers might look modest on paper. The context around them is anything but.

The Hong Kong market was closed for a public holiday, so Wednesday's action played out entirely on the mainland - and it was telling on its own.

The Factory Data Behind China's Market Gains

A business survey published Wednesday confirmed that China's manufacturing sector expanded for a seventh consecutive month in June, completing the strongest quarter for Chinese manufacturing since late 2020. Seven months. In a row. That's a trend, not noise.

If you've been following the China Manufacturing Pmi June What The Re numbers closely, Wednesday's survey fits exactly what the return to expansion territory was signaling several months ago. Orders are moving. Factories are running. Investors had a fundamental anchor to point at - and they used it.

That said, manufacturing expansion doesn't automatically fix everything else. Consumer confidence, property prices, youth employment - those are different problems. But in a market hungry for positive signals, China manufacturing completing its strongest quarter since late 2020 was enough to push buyers into action.

Tech Leads as China Stocks Rise on Robust Activity Data

The headline index moves were solid. The real energy was in tech - and it was sharp.

An index tracking chipmaking equipment and materials jumped nearly 4 percent on Wednesday to fresh record highs. Chip equipment indices hitting fresh record highs isn't just a one-day trade. It's a signal about long-term industrial direction, about where China's investment in semiconductor independence is actually going. Biotech stocks gained. Software stocks gained. The China manufacturing sector expansion for a seventh straight month gave institutional investors the macro cover they needed to build on those positions.

Innovative sectors including biotech and software Startups have been among the clearest beneficiaries of Beijing's policy tilt toward what it calls "new productive forces." Wednesday's moves reflected that alignment almost perfectly.

From a Science and research standpoint, the chipmaking breakthroughs behind that 4 percent sector surge have implications well beyond what shows up on a stock ticker. And China's hardware ambitions extend further still - if you want a sense of how deep the next-generation technology investment goes, the piece on China Just Rolled Out The Quantumctek Ez dilution refrigerator shows the kind of infrastructure bet Beijing is making.

Why tech shares are outperforming traditional sectors in China right now comes down to one clear alignment: policy direction and market positioning are pointing the same way. That doesn't last forever - but right now, it's working.

What Xi Jinping's Speech Actually Told the Market

President Xi pledged on Wednesday to "steadily promote high-quality development." This isn't vague inspiration - it's deliberate, repeated policy language referring to sustainable, innovation-driven growth rather than the old model of debt-fueled infrastructure expansion.

The impact of Xi Jinping's sustainable innovation-driven growth pledge shows up clearly in which sectors responded. Not general infrastructure. Not broad property. Chipmaking, biotech, and software - exactly the sectors Xi's framing elevates. Markets are reading Beijing's priorities correctly.

And when policy direction and earnings momentum align, institutional money tends to follow.

Goldman Sounds Cautious - Here's Why That Matters

Not everyone is optimistic. Honestly, that's healthy.

Goldman Sachs published a note this week summarizing meetings with Chinese investors over the past several days. The consensus among local clients? More cautious on near-term China growth momentum than the positive PMI data might suggest. Goldman described it as a "more bifurcated growth mix" - two economies running at different speeds simultaneously.

Discussions focused on fragile consumer confidence amid labor market pressures and the negative wealth effect from the ongoing property downturn in China. Property prices are still dragging on household wealth. People who feel less wealthy spend less. That headwind doesn't disappear because the factory floor is busy.

The Goldman Sachs cautious note on China near-term growth momentum isn't a sell signal - it's a "know what you're actually buying" signal. Bifurcated growth mirroring the real economy in Chinese stocks means sector selection matters more than simply going long a broad index. You can't own everything and call it a thesis.

Traditional Sectors Joined the Rally Too

Here's what got less attention on Wednesday: it wasn't only tech that moved.

Agriculture stocks rose sharply. Property stocks rose sharply. Broadening interest from investors in Chinese traditional sectors like these suggests something beyond a pure narrative trade in innovation stocks. When capital starts rotating into areas that had been largely overlooked, it can signal a wider floor forming under the market.

Software stocks rising makes sense if you follow the Webdev and digital infrastructure push in China closely. Beijing has been explicitly backing domestic software development for years - this is policy-backed demand, not speculation.

M&G Makes the Case for Growth, Not Just Defense

"We see a lot of growth on offer at better than reasonable prices in China across sectors. So, this is not just a defensive allocation of capital for us."

That's Vikas Pershad, portfolio manager for Asian Equities at M&G Investments. The key phrase is "not just defensive." A lot of Western allocators still frame their China positions as a hedge - hold a low weight, diversify away from developed markets, wait for clarity that never quite arrives. Pershad is saying something different: the earnings and valuations are justifying the allocation of capital in Asian equities on their own terms.

"We'll see in a few years if the earnings and valuations have justified that allocation of capital. But we think it does, which is why we've done that."

Straightforward. And notably, M&G's position spans sectors - it's not just the obvious tech plays. That kind of breadth, from a major fund manager, is a meaningful signal about where genuine conviction is forming. Growth on offer at better than reasonable prices in China is a thesis, not a guarantee. But it's a considered one.

What to Watch as This Story Develops

The Security dimensions of China's chip push are hard to ignore as chipmaking equipment stocks hit record highs. Geopolitical questions around technology access don't vanish because a domestic index moved up - if you're building China equity exposure, that variable belongs in your analysis.

The Gadgets and consumer electronics side of the economy is more directly tied to domestic confidence. When consumer sentiment is fragile - as Goldman flagged - even strong hardware producers eventually feel the downstream effect. Factory output and retail demand are not the same thing.

For tracking how artificial intelligence investment intersects with China's innovation agenda, the Ai coverage is worth bookmarking. Use Search to pull up more focused China market reporting, or head to Www.Globalbyte.News for ongoing coverage where technology, markets, and global economic trends connect.

Pulling It Together

China stocks rise on robust factory activity data - and Wednesday made the case more clearly than most recent sessions. Tech at record highs. Traditional sectors broadening. Goldman cautious on near-term momentum. M&G bullish on valuations across sectors. Xi pledging innovation-driven growth.

None of those views contradict each other. They're describing different parts of the same market, at the same moment. The two-speed growth mirroring China's real economy in Chinese stocks isn't going to resolve quickly - and that's fine, provided you know which speed you're riding.

Manufacturing expansion completing its strongest quarter since late 2020 is a real foundation. Whether consumer confidence and property values eventually catch up to that is the bigger question for the second half of 2025. Watch the breadth. Watch whether Wednesday's traditional sector gains hold. And watch what Goldman's Chinese clients do next - because local sentiment, more often than not, leads the data.