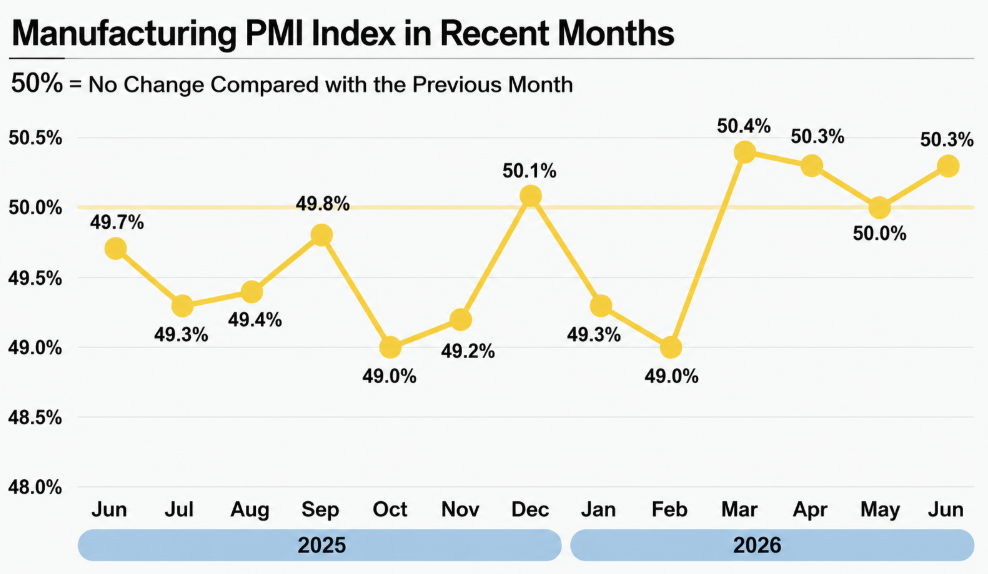

June's official data is in. China’s manufacturing PMI expansion territory is confirmed - the manufacturing PMI climbed to 50.3%, the non-manufacturing business activity index reached 50.2%, and the composite PMI output index hit 50.6%, a new high for 2025. All three core indices crossed above the 50-point boom-bust threshold simultaneously, all rising month-on-month. Analysts at outlets like Securities Times and CITIC Securities flagged the composite output index reaching a new high as the most significant milestone in the release.

So yes, this is a positive reading. But what sits underneath the headline numbers is worth understanding carefully before drawing big conclusions.

China's Manufacturing PMI returned to expansion territory in June 2026, reflecting stronger factory activity, improving business confidence, and renewed economic momentum.

Why This PMI Reading Carries More Weight Than Usual

One month above 50 can be noise. What makes this China manufacturing PMI June expansion territory reading harder to dismiss is the Q2 average. Both manufacturing and non-manufacturing improved versus Q1. That's directional momentum, not a one-off bounce.

The composite PMI output index reaching a new year-high matters because of context. External pressure hasn't gone away - geopolitical friction, global supply chain disruption, trade policy uncertainty. The index pushing higher anyway signals economic resilience and stabilizing market expectations. It doesn't guarantee a smooth second half. But it gives H2 a foundation.

High-Tech Manufacturing Is Running Well Ahead of the Pack

Not all manufacturers are sharing the same recovery. High-tech manufacturing PMI growth momentum is clearly visible in the data: high-tech manufacturing PMI reached 53.5%, more than 3 points above the overall level. Equipment manufacturing and consumer goods improved their business climate simultaneously. Energy-intensive industries remain in contraction territory. The gap between old and new growth drivers has rarely been this stark in a single month's data.

Computer, communications, electronics, and specialized equipment manufacturers are all operating at elevated activity levels. Sustained AI demand and high-end equipment production are driving it. The kind of China tech investment flowing into AI agents and next-generation hardware is feeding directly into these PMI figures. And the build-out of domestic chip supply chains - including multi-billion dollar DRAM supply agreements - is translating into measurable production activity.

This is what the transition from old to new growth drivers actually looks like in the numbers. Not a narrative. Evidence.

New Orders Bounced Back - And Export Demand Surprised

The new orders index jumped 1.3 percentage points from May, returning to expansion after two months below the boom-bust line. A move that size in a single month suggests real demand improvement, not seasonal adjustment.

The export side was the bigger surprise. New export orders index economic resilience showed up clearly: it crossed back above the expansion threshold, signaling that external demand is stabilizing after a rough patch. Given everything happening with global supply chains and geopolitical uncertainty, that wasn't guaranteed. Exports holding up - even modestly - matter a lot for sustaining manufacturing sector momentum heading into Q3.

Production and demand are expanding in parallel. Both the production index and the new orders index rose. That combination provides durable support for continued PMI improvement rather than a one-month pop that reverses quickly.

Services: The Recovery People Aren't Talking About Enough

The non-manufacturing business activity index recovery tends to get overshadowed by manufacturing data. It shouldn't. The service sector business activity index has risen for two consecutive months, and the quality of that recovery matters as much as the direction.

Telecommunications and broadcasting activity indices above 55% are among the strongest sub-sector readings in the entire economy right now. Internet software and information technology services are running at similar levels. New growth drivers in the information service industry aren't just holding up - they're expanding fast. AI, big data, and cloud computing are integrating with productive services demand in ways that show up directly in these sub-sector figures.

You can see it at the company level too. Meituan’s AI model expansion into trillion-parameter territory reflects the kind of private-sector AI investment that generates sustained demand across information services. Chinese open source adoption is extending that momentum beyond China's borders, reshaping technology markets on multiple continents.

A digitally-driven, new-driver-led expansion pattern in non-manufacturing is taking shape. That's a structural shift, not a monthly reading.

Construction: Still Below the Line, But Something Is Shifting

Construction remains below the 50-point threshold. The real estate sector adjustment is ongoing, and it won't resolve quickly. Honest assessment: the construction business activity index has real structural headwinds right now.

But within that picture, something is changing. The construction expectations index is in expansion. Six networks planning and construction infrastructure orders are accumulating as major projects accelerate their timelines. Ultra-long-term special treasury bonds and special-purpose bonds are being issued and deployed - and that money eventually converts into project starts and construction activity. The build-out of Chinese supercomputing infrastructure - full-stack heterogeneous computing platforms at national scale - represents exactly the kind of high-specification infrastructure spend that flows through to construction PMI over time.

If bond deployment continues at pace, the H2 construction outlook looks cautiously better.

Costs Are Easing, and for Manufacturers That's a Big Deal

Here's a development that doesn't make headlines but should. The raw material purchase price index deflationary easing arrived clearly in June: both the major raw material purchase price index and the ex-factory price index fell noticeably.

Imported price pressure from high international commodity prices has given manufacturers real breathing room. A relative stabilization in Middle East tensions guided energy market expectations lower. For midstream and downstream manufacturing enterprises caught between rising upstream costs and weak end-market pricing power, this is meaningful relief. Lower purchase prices improve cost structures. Better cost structures improve profit expectations. And that improves the willingness and ability of midstream enterprises to replenish inventories - which, if it materializes, supports production volumes in Q3.

This may not last. But right now, the pressure is off.

The Structural Divide Nobody Should Gloss Over

Here's where the honest assessment gets uncomfortable. China manufacturing PMI June expansion territory is real. The recovery is also concentrated.

Growth is flowing primarily to high-value-added industries and large leading enterprises. SMEs and traditional industries are still struggling with weak end-user demand, transformation pressure, and sluggish demand transmission through legacy supply chains. Micro and small enterprises especially - their confidence in business recovery needs direct policy attention, not just indirect benefit from aggregate PMI improvement.

The China startups sector faces its own version of this divide, and China science and industry broadly needs coordinated support to ensure high-tech gains don't paper over persistent weakness elsewhere. The progress in China quantum technology output - including advanced dilution refrigerators and quantum hardware - shows what focused investment delivers at the high end. Getting that same intentionality to work for SMEs in traditional sectors is the harder, more consequential policy challenge.

Proactive fiscal policies and moderately loose monetary policies create the conditions for confidence to rebuild. But targeted interventions - expanding market channels for SMEs, clearing bottlenecks in traditional industrial chains, and funding digital transformation of traditional industries - are what turns aggregate PMI recovery into a broadly felt one. The boom-bust line separation index numbers look positive in aggregate. Getting the benefits distributed evenly takes deliberate effort over time.