Three Korean startups walked into Electronica Shanghai 2026 with something to prove. Not prototypes. Not aspirational roadmaps. Real products - inference chips, physical AI accelerators, a software LLM booster - pointed directly at the companies building the world's cars, appliances, robots, and data centers.

If you've been following AI semiconductor coverage closely, this move won't surprise you. But the specifics of what Korean fabless chipmakers brought to Electronica Shanghai 2026 - and who they're targeting - are worth paying attention to. China concentrates automotive, home appliance, and data center semiconductor demand at a scale that doesn't exist anywhere else. Mass production cycles are fast. Decision-making is faster. For nimble foreign startups, that's a window.

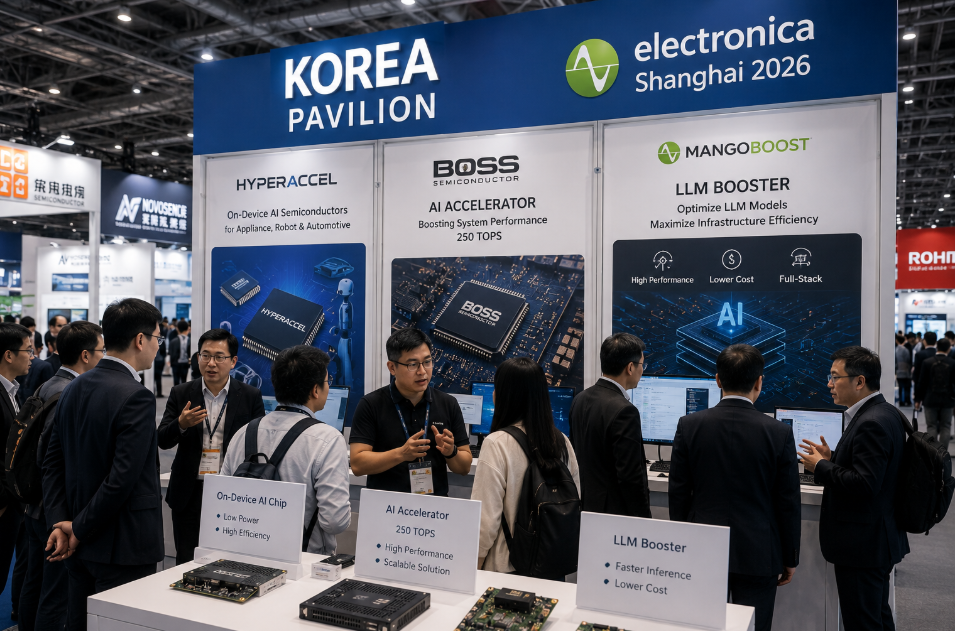

Why the Korea Pavilion at Electronica Shanghai Made Strategic Sense in 2026

Honestly, the math isn't complicated.

Chinese local fabless competition is growing, and nobody at the Korea pavilion pretended otherwise. But large domestic players have a structural problem: too many customers, not enough bandwidth for one-on-one support. Korean fabless chipmakers at Electronica Shanghai 2026 were positioning directly in that gap - customization, speed, agile technical engagement.

The trade environment helps explain the timing too. An open trade approach with China is gaining traction across several markets, and China trade consultations 2026 between major trading blocs are keeping access pathways open. Companies that build Chinese supplier relationships now get established before the market consolidates around domestic alternatives.

All three companies said something similar: Korea can't offer this kind of demand. China can.

HyperAccel: Low-Power Edge AI Chips Built for How China's Market Actually Works

HyperAccel's core product line covers data center inference chips. But in Shanghai, the pitch changed. Server-form products were on display alongside an on-device AI chip scheduled to ship later this year.

The target verticals are broad - appliances, robots, automotive. They all share one requirement: AI that runs locally, without constant cloud connectivity, without draining a battery. On-device is the only architecture that fits.

Here's where the market alignment gets interesting. How HyperAccel leverages LPDDR memory for low-power edge AI chips isn't just a product feature - it's a strategic match with how Chinese manufacturers build. China's market heavily favors low-power double data rate (LPDDR) memory over high-bandwidth memory (HBM). It's a market-wide preference that shapes system design from the ground up. HyperAccel's chip was designed around LPDDR constraints from the start, not retrofitted to fit them. That's not a minor distinction when you're selling to manufacturers who've already standardized their memory stack.

HyperAccel managers So-young Park and Tae-seo Eom confirmed active post-show conversations with multiple companies - both local Chinese players and foreign firms operating in China. Testing discussions are ongoing. "The chip itself is highly efficient," one official noted. "It will fit well with the Chinese market, which mainly uses LPDDR."

The company left Shanghai with more than contacts. It left with a case for continued engagement.

Boss Semiconductor's 250 TOPS Accelerator - This Was Their Third Time in China

Boss Semiconductor's pitch is disarmingly simple. Take the 250 TOPS AI accelerator. Attach it to whatever system the customer already runs. Expand AI performance without requiring a platform overhaul. No rip-and-replace.

That low-friction approach appeals to Chinese OEMs and physical AI companies specifically, which explains why this was Boss Semiconductor's third China trade appearance in one cycle. After Auto Shanghai last year and Auto Beijing earlier in 2026, the company showed up at Electronica Shanghai with a local sales representative already in place and regular conference calls already running with prospective OEM customers. That's not exploratory attendance. That's pipeline-building.

Understanding Boss Semiconductor's 250 TOPS accelerator architecture for physical AI comes down to two things: chiplet design and startup-grade support. Global semiconductor companies have too many accounts to give smaller customers real technical engagement. Boss Semiconductor makes that gap its main selling point. Agile support, fast customization cycles, actual responsiveness.

The product range spans high-end 250 TOPS-class systems and lower-end options for cost-sensitive segments. But specs aren't the real differentiator - customization speed is. That kind of flexibility is what separates an active hardware startup ecosystem from the incumbents it's competing against.

"China's market, with fast mass-production cycles and decision-making, fits well with the characteristics of startups whose strength is fast response," one official said. The company plans to keep expanding in China as part of a broader global market strategy.

MangoBoost: A Software LLM Booster That Makes Non-Nvidia Hardware Worth Running

MangoBoost's first Electronica Shanghai appearance was partly about listening. But the company didn't show up empty-handed.

Its full-stack infrastructure optimization solution targets a problem that chipmakers typically gloss over: the gap between chip benchmark performance and actual system throughput once data transmission, storage, and processing bottlenecks enter the picture. Faster chips don't automatically mean faster systems. MangoBoost argues that the software layer is where the real efficiency gains are being left on the table.

The specific product for China is a software LLM booster. By pushing open-source inference engine optimization to its limits, MangoBoost claims 2-3x improvements in LLM processing speed on the same hardware setup. Finding affordable Nvidia alternatives using MangoBoost software and AMD GPUs is exactly the use case it leads with. "We can deliver results with lower usage costs than Nvidia while achieving high performance," an official said. For customers where Nvidia supply is constrained - or where the cost equation just doesn't work - that's a genuinely useful option.

Near-term, MangoBoost plans to build relationships with Chinese AI software service providers before pushing the full hardware offering. Given China's open-source AI rise and the increasingly active China AI model landscape, getting embedded in the software ecosystem before pushing hardware products is a sensible sequence. Server-form inference hardware inquiries are already coming in locally. That side may accelerate on its own.

What the Korea Pavilion at Electronica Shanghai 2026 Actually Signals

Korean chipmakers at Electronica Shanghai 2026 weren't there to learn about the market. They came with production-ready products, repeat China appearances, and active customer conversations in progress.

The context keeps getting more significant. China's AI chip ecosystem is maturing at a pace that's outstripping what any single domestic supplier can cover. China's computing ambitions are expanding well beyond consumer AI, reaching into industrial infrastructure and physical AI. And the broader wave of 2026 tech expo innovations across the region is shortening how long buyers deliberate before making sourcing decisions.

All three companies left Shanghai with active leads. Whether those convert to production contracts depends on execution - and on how quickly Chinese OEM supply chains move once testing begins. Given the pace of that market, don't expect a long wait.